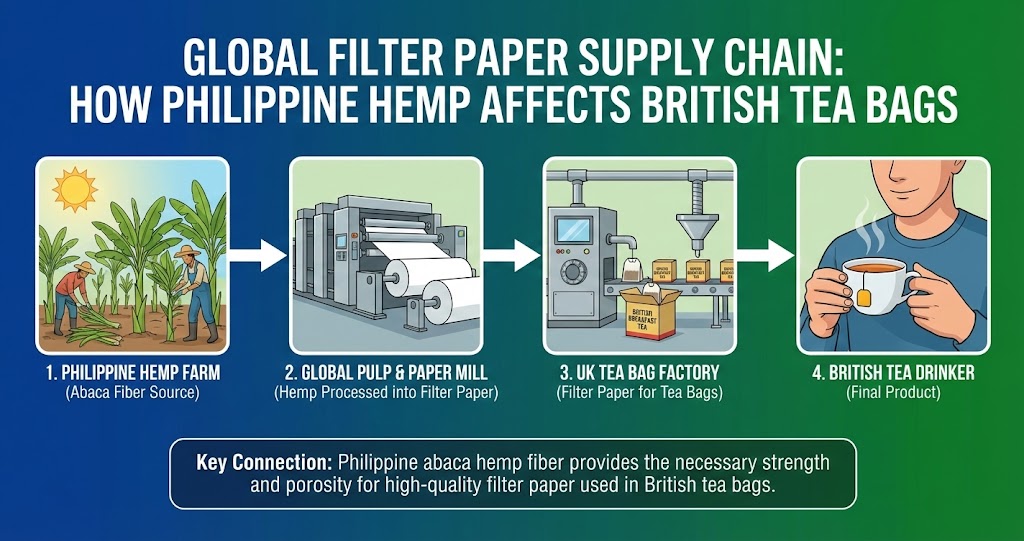

1. Abaca Hemp: The 85% Philippine Monopoly on Tea Bag Fiber

What is abaca (Manila hemp)? Botanical source: Musa textilis (banana family relative—NOT true hemp Cannabis sativa, "Manila hemp" misnomer from rope trade history), fiber characteristics (exceptional wet strength—retains 80-90% tensile strength when wet vs. 30-40% wood pulp, critical for tea bag immersion boiling water, naturally heat-sealable without synthetic binders), grown exclusively tropical climates (Philippines 85% global production ~60,000-70,000 tonnes annually, Ecuador 10-12%, Costa Rica/Indonesia <5% combined, see supply concentration risks). Why abaca dominates tea bag paper: No viable alternatives at scale (wood pulp requires chemical strengthening agents—affects taste purity, synthetics like nylon—consumer backlash against plastic in tea, abaca "natural" + functional monopoly), food-grade certification (FDA/EU regulations require taste-neutral fibers—abaca naturally meets standards, substitutes face expensive testing + reformulation), processing heritage (Philippine abaca industry 150+ years—infrastructure + expertise concentrated Mindanao/Leyte regions, new entrants face 5-10 year ramp to quality).

Philippine production dynamics: Smallholder farming model (70-80% production from 1-3 hectare family farms—NOT plantation scale, labor-intensive harvest requires manual stripping fiber from stalks, 120-150 labor days per hectare vs. 20-30 days mechanized crops), regional concentration (Davao/Bukidnon/Leyte provinces—volcanic soil + rainfall 2,000-3,000mm annually ideal, Typhoon Alley vulnerability major supply risk, 2013 Typhoon Haiyan destroyed 30-40% abaca crop caused 6-month global tea bag shortage + 35% price spike). Price volatility patterns: Baseline pricing ($1,200-1,600 per tonne fiber 2015-2019—stable when weather normal, translates to 0.15-0.25p per tea bag filter paper cost, see tea bag cost breakdown), weather-driven spikes (2020 typhoons + COVID labor shortage—prices hit $2,200-2,600/tonne 40-60% increase, packers absorbed most cost increase retail tea prices rose only 5-8%, lag effect 6-12 months as contracts rolled over).

2. Tea Bag Manufacturing Economics: The 0.2p Paper Component

Cost buildup from fiber to finished bag: Raw abaca fiber to paper rolls ($1,500/tonne fiber → $3,000-4,000/tonne finished filter paper—pulping + bleaching + rolling adds 100-150% conversion cost, specialized mills in Germany/UK/Netherlands produce 80% of global tea bag paper despite Philippine fiber source), paper to cut tea bags ($3,500/tonne paper = ~$0.18-0.25p per tea bag filter—assumes 5-7cm² bag, 50-60g/m² paper weight, heat-seal edges without string for economy bags), string + tag premium (adds 0.03-0.05p per bag—cotton string + paper tag, premium brands only, supermarket own-label skip to save cost, see cost component analysis). Total filter paper economics in £2 box: 80 tea bags × 0.20p average = 16p total paper cost, represents 8-10% of £2 retail price (or 10-12% of packer cost £1.30-1.50, minor component but supply disruption cascades through entire chain).

| Supply Chain Stage | Cost per Tonne | Value Add | Major Players | Bottleneck Risk |

|---|---|---|---|---|

| Abaca Fiber (Raw) | $1,200-1,600 | — | Philippine smallholders (70-80%) | HIGH (typhoon/pest vulnerability) |

| Fiber Processing (Dried/Graded) | $1,500-2,000 | +15-25% | Regional processors (Davao/Leyte) | MEDIUM (capacity limited 5-8 major mills) |

| Filter Paper Manufacturing | $3,000-4,000 | +100-150% | Glatfelter/Purico/Terranova (Germany/Netherlands) | LOW (excess capacity normally 20-30%) |

| Tea Bag Packing | £0.20p per bag | +assembly labor/machinery | Unilever/Taylors/Typhoo factories (UK) | LOW (multiple contract packers available) |

Alternative materials exploration: Wood pulp blends (abaca 70% + wood pulp 30%—reduces cost 15-20% but wet strength compromised, "bag breakage in cup" consumer complaints, most packers abandoned after 1990s trials), synthetic fibers (PLA/nylon) (polylactic acid corn-based—"biodegradable plastic", 2010s Twinings/Clipper trials faced consumer backlash "microplastics in tea" health fears, regulatory uncertainty EU/UK, mostly withdrawn despite superior heat-seal properties), why abaca persists despite cost (natural + functional + regulatory-proven—safest choice for brands, switching cost $2-5M per production line for equipment retooling, risk of consumer rejection not worth 10-15% paper savings when tea bags already 1.0-1.35p total cost).

3. The 2013 Typhoon Haiyan Supply Shock: Case Study in Fragility

Pre-typhoon market (2010-2013): Stable abaca pricing ($1,300-1,500/tonne—predictable costs, packers contracted 6-12 months forward eliminating spot volatility), inventory levels low (just-in-time manufacturing—2-4 weeks filter paper stock typical, cost of capital minimization, vulnerability to disruption unrecognized). Typhoon Haiyan impact (November 2013): Devastation scale (Category 5 storm—Leyte/Samar provinces 90% abaca crop destroyed, 30-40% national production offline, 6,000+ deaths humanitarian crisis overshadowed economic impact), immediate price response (spot fiber prices $1,400 → $2,100/tonne within 3 weeks 50% spike—panic buying by paper mills, tea packers scrambling to secure 6-month supply before stocks depleted, see commodity price shocks).

Industry response and mitigation: Short-term rationing (January-June 2014—Unilever/Twinings prioritized core SKUs, specialty/gift products delayed or reformulated to use less bags, "100-bag packs" replaced with "80-bag" temporarily to stretch paper supply), quality degradation acceptance (paper mills blended higher wood pulp ratios—35-40% vs. normal 20-25%, increased bag breakage complaints +15-20% but avoided stockouts, brand reputation hit accepted as lesser evil than empty shelves). Price passthrough to consumers: Delayed impact (retail tea bag prices rose 5-8% March-September 2014—6-12 month lag as contracts rolled, packer margins compressed 20-30% interim period absorbed shock, see margin dynamics), private label hit harder (supermarket own-label—less pricing power absorbed 60-70% of cost increase, branded tea PG Tips/Tetley passed through 80-90% to consumers via "commodity cost adjustment" justification).

Why Major Packers Don't Vertically Integrate Abaca Supply

Scale mismatch problem: Unilever tea bag volume (30-40 billion bags annually globally—requires 15,000-20,000 tonnes filter paper, but 20,000-25,000 tonnes abaca fiber raw material due to processing losses), vs. Philippine smallholder model (60,000 tonne national production from 30,000+ family farms 1-3 hectares—impossible to consolidate without displacing entire regional economy, land reform laws prevent foreign ownership large plantations). Economic barriers to plantation model: Labor cost structure (manual fiber stripping—120-150 days per hectare, Philippine rural wages $8-12/day competitive, mechanization attempts failed fiber quality suffers machine damage, plantation wages $15-25/day would destroy economics), typhoon risk concentration (owning 5,000-10,000 hectare plantation—single storm wipes out 80-90% of investment, diversified smallholder sourcing spreads risk across regions, insurance unavailable or prohibitively expensive for abaca monoculture). Expertise barrier: Tea companies lack agricultural competency (Unilever/Twinings core skills—brand marketing + distribution, abaca farming requires different expertise soil science/pest management/fiber processing, 10-15 year learning curve to match local knowledge), better to manage supplier relationships (long-term contracts with Philippine processors—lock pricing 12-24 months forward, strategic inventory 3-6 months paper stock vs. 2-4 weeks pre-2013, accept occasional supply shocks as cost of specialization, see supply chain relationship models).

4. Heat-Seal Technology: Why Tea Bags Don't Need Glue Anymore

Traditional glue-sealed bags (pre-1990s): Construction method (abaca paper folded—edges sealed with food-grade adhesive, required drying time + quality control to prevent glue taste contamination), consumer concerns (1980s health scares—"glue in tea" headlines, some adhesives contained formaldehyde traces, regulatory pressure + brand reputation risk drove innovation). Heat-seal evolution: Thermoplastic abaca treatment (paper coated with thin polypropylene layer—melts at 160-180°C creates seal without adhesive, heat-seal bars in packaging machinery 0.5-1 second press time seals edges), machinery investment (heat-seal packaging lines—$2-5M per line vs. $0.5-1.5M glue-based, higher upfront cost but 30-40% faster throughput + eliminates adhesive supply chain, ROI 3-5 years for high-volume packers).

Heat-seal advantages: Taste purity (zero adhesive contamination—addresses 1980s concerns, "natural" marketing claim reinforced even though polypropylene coating technically plastic, consumer perception "heat-sealed" = safer than "glued"), production speed (600-800 bags per minute heat-seal—vs. 400-500 glue-based due to drying time, 50% throughput increase drives down labor cost per bag from 0.12p to 0.08p, see manufacturing cost breakdown). Biodegradability tradeoff: Polypropylene coating problem (pure abaca paper—biodegrades 6-12 months, heat-seal coating—delays breakdown to 18-36 months, not truly "plastic-free" despite marketing, 2018-2020 consumer backlash led to new innovation wave), next-generation solutions (PLA plant-based coating—Clipper/Pukka 2019-2020 launches, biodegrades 12-18 months but 20-30% higher cost + regulatory uncertainty, ultrasonic sealing no coating—experimental 2020s technology, equipment cost prohibitive $8-12M per line limits adoption to premium brands only).

5. String vs. Stringless: The 0.03p Decision That Shapes User Experience

String + tag economics: Component costs (cotton string 12-15cm—0.015-0.02p per bag, paper tag 2×3cm—0.01-0.015p, metal staple—0.002-0.003p, total add-on 0.027-0.038p per bag), assembly complexity (string attachment—requires additional machinery station, slows packaging line 15-20%, labor + equipment cost adds another 0.005-0.01p, total string premium 0.03-0.05p vs. stringless). Market segmentation by string: Premium brands string preference (Twinings/Tetley/PG Tips—consumer expects string for ease of bag removal, brand differentiation "quality tea has string", 0.05p cost absorbed in £4-5 per box premium pricing), supermarket own-label stringless (Tesco/Asda value tea—no string saves 0.03-0.05p per bag × 80 bags = 2.4-4.0p per box, significant savings on £1.50-2.00 product where 10% margin compression critical, see private label economics).

Consumer behavior impact: String removal convenience (grab tag pull out bag—vs. stringless requires spoon or finger fishing in hot water, minor inconvenience but real usability difference), willingness to pay for string (consumer surveys—45-55% "prefer string" but only 20-25% willing to pay 10-15% premium for it, explains why premium brands include string but value brands skip, price-conscious buyers accept tradeoff). Specialty formats niche markets: Pyramid bags (nylon/PLA mesh—no string but large footprint easy to grab, premium positioning $0.08-0.15 per bag vs. standard $0.015-0.025, whole-leaf tea visibility justifies cost, see leaf presentation value), drawstring sachets (loose tea in sealed sachet + drawstring—combines loose-leaf quality with bag convenience, 0.12-0.20p per sachet, ultra-premium niche <5% market share, T2/Fortnum & Mason positioning).

6. Biodegradability Economics: The Premium for Compostable Tea Bags

Traditional heat-seal bags biodegradation: Polypropylene coating persistence (abaca fiber breaks down 6-12 months—but PP coating remains 5-10 years, creates "microplastic residue" in compost, 2017-2019 consumer investigations BBC/Which?—"tea bags contain plastic" headlines damaged category reputation), composting facility rejection (industrial composters—began rejecting tea waste 2018-2020 due to plastic contamination, home composters frustrated by persistent bag skeletons, brand pressure to reformulate). Fully compostable alternatives development: PLA (polylactic acid) coating (plant-derived polymer—corn/sugarcane feedstock, biodegrades 12-24 months industrial composting conditions, meets EN13432 compostability standard), PLA cost premium ($4,500-6,000/tonne vs. $3,000-4,000 PP-coated abaca paper—40-60% higher material cost, adds 0.05-0.08p per bag, absorbed by premium brands Clipper/Pukka or passed to consumers via 10-15% retail price increase).

| Tea Bag Type | Filter Cost (p per bag) | Biodegradation Time | Compostability Standard | Market Share % |

|---|---|---|---|---|

| Traditional Heat-Seal (PP coating) | 0.18-0.25p | 5-10 years (coating persists) | NOT compostable (plastic residue) | 60-70% (declining) |

| PLA-Coated (Plant-Based) | 0.25-0.35p | 12-24 months (industrial composting) | EN13432 certified compostable | 20-30% (growing 15-20% annually) |

| Ultrasonic Seal (No Coating) | 0.30-0.45p | 6-12 months (pure abaca) | Fully biodegradable (no additives) | 5-10% (premium only) |

| Loose Leaf (No Bag) | 0p (no filter) | Immediate (pure tea leaf) | Fully compostable | 5% (niche enthusiasts) |

Regulatory pressure timeline: 2018 UK government inquiry: Plastic in tea bags investigation (DEFRA/Parliament committee—consumer group petitions 100,000+ signatures, major brands pledged elimination by 2020-2023), 2020-2023 reformulation wave (PG Tips 2020—switched PLA coating, Twinings 2021, Yorkshire Tea 2022, 70-80% major brands converted by 2023, laggards face consumer boycott risk + regulatory penalties), cost absorption strategies (most brands absorbed 0.05-0.08p per bag increase—maintained retail prices to avoid market share loss, packer margins compressed 10-15% accepted as cost of maintaining brand equity, see competitive pricing dynamics). Greenwashing concerns: PLA industrial composting requirement (home composters too cool—PLA needs 55-60°C for breakdown, <10% UK households have access to industrial composting collection, "compostable" marketing misleading if ends up landfill where PLA persists 20-50+ years like conventional plastic), ultrasonic seal true solution (but 50-80% cost premium limits to ultra-premium brands—Rare Tea Company/Jing, mass market unlikely to adopt unless regulation mandates + consumer willing to pay £0.30-0.50 more per box).

7. Future Supply Chain Diversification: Can Ecuador/Costa Rica Replace Philippines?

Ecuador abaca sector (10-12% global production): Production scale (6,000-8,000 tonnes annually—vs. Philippines 60,000-70,000 tonnes, Ecuador concentrated Esmeraldas/Manabí provinces, smaller farm scale 0.5-2 hectares), quality comparison (fiber tensile strength 10-15% lower—due to soil/climate differences, acceptable for tea bag paper but commands 10-15% price discount vs. Philippine equivalent, Ecuador fiber $1,200-1,400/tonne vs. Philippine $1,400-1,600). Expansion potential limited: Land competition (banana/cacao more profitable—farmers prioritize export crops, abaca niche product, difficult to scale beyond 10,000-12,000 tonnes without major price incentives), infrastructure gaps (fiber processing—only 3-4 major mills vs. Philippines 15-20, capacity bottleneck limits ability to absorb demand surge even if farming scales, see supply chain concentration).

Costa Rica/Indonesia minor producers: Costa Rica 1,500-2,500 tonnes (highest quality fiber—volcanic soil produces exceptional strength, but tiny scale limits to specialty applications, expansion constrained by land costs + environmental regulations protecting rainforest), Indonesia 1,000-2,000 tonnes (Sulawesi/Sumatra—suitable climate but farmer expertise lacking, quality inconsistent, government promotion programs 2015-2020 failed to scale due to competing palm oil profitability). Realistic diversification outlook: Philippines dominance likely persists (80-85% market share probable through 2030—scale + expertise + infrastructure advantages insurmountable, Ecuador may grow to 15-18% if major typhoon disrupts Philippines creating opportunity), strategic inventory vs. supply diversification (tea packers post-2013—increased paper stock from 2-4 weeks to 12-16 weeks, 3-4 month buffer cheaper than attempting to develop alternative supply chains, accept Philippine concentration as manageable risk with inventory cushion, see supply chain risk management).

Comments